Cement + CCUS Outlook 2025

Lower-clinker recipes and smart carbon capture are now the two levers every kiln in India and the Gulf must pull

1 Why cement is still a climate outlier

Ordinary Portland cement (OPC) releases 0.55 – 0.90 t CO₂ t⁻¹ because limestone is literally baked out of its carbon. Two levers dominate any credible plan:

- Lower the clinker-to-cement ratio (C/C). Swap in fly-ash, slag or calcined clay.

- Capture what remains. Even an aggressive blend leaves > 50 % “process CO₂” that only CCUS—or new chemistries still at pilot scale—can eliminate.

A new CEEW study backs that up: 56 % of residual emissions from India’s steel-and-cement complex remain “hard” even after energy-efficiency and alternative fuel shifts, so CCUS isn’t optional.

Planning a capture-ready kiln?

- Book a 30 min kiln call-back

- e-mail sales@ssgaslab.com

- or dial +91-124-46 XXXXX

2 2025 policy pressure—no more wiggle room

| Jurisdiction | 2025 change | Impact |

|---|---|---|

| India – BIS draft amendment to IS 269 | Signals medium-term C/C ≤ 0.65 for OPC-43 by 2026. | Pushes manufacturers toward blended cements and capture for residual kiln gas. |

| UAE – Net-Zero 2050 Strategy (rev. Jan 2025) | Tags cement a “priority hard-to-abate” sector; fast-track permits for plants adding CCUS or WHR. | Couples licensing speed to capture commitments; interim goal 14 Mt CO₂ y⁻¹ captured by 2030. |

Combined, these rules force plants to address the remaining 56 % hard CO₂ the CEEW model highlights.

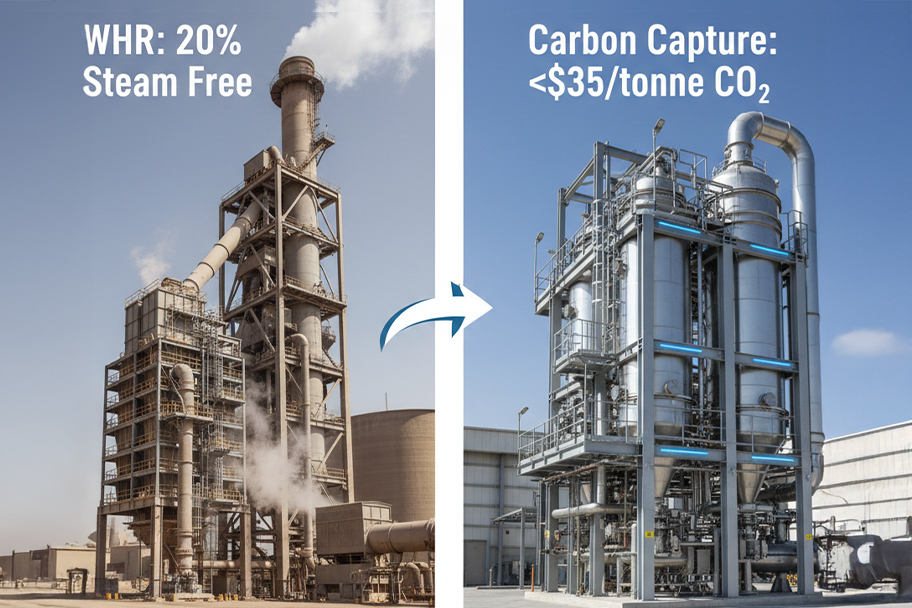

3 Waste-heat recovery: capture’s cheapest ally

Dry-process kilns vent 200–350 °C gas. Sharjah Cement’s 9 MW WHR unit already avoids ≈ 70 000 t CO₂ y⁻¹ and can feed half the steam for a 0.15 Mt y⁻¹ capture skid. Field data show WHR + capture cuts external steam up to 20 %.

Need a quick WHR + capture pay-back?

- Talk to our cement specialist

- e-mail sales@ssgaslab.com

- or call +91-124-46 XXXXX

4 What 2025 capture economics really look like

| Capture scope | Installed CAPEX* | OPEX band | Net cost after tax shields† |

|---|---|---|---|

| 0.4 Mt y⁻¹ retrofit | US $120–160 M | US $17–22 t⁻¹ | US $35–55 t⁻¹ CO₂ |

| 0.1 Mt y⁻¹ modular skid | US $60–70 M | US $22–28 t⁻¹ | US $45–60 t⁻¹ CO₂ |

*Includes WHR tie-ins; excludes pipeline.

†India 40 % Y1 depreciation or UAE 50 % two-year write-off; aligns with IEA curves.

5 India vs UAE — two divergent but real trajectories

| Metric | Andhra Pradesh blended line | Ras Al Khaimah integrated plant |

|---|---|---|

| Starting C/C | 0.78 | 0.75 |

| 2026 target C/C | 0.66 | 0.70 |

| Planned capture | 0.12 Mt y⁻¹ (kiln stack) | 0.15 Mt y⁻¹ (pre-calciner + kiln) |

| Steam source | 100 % WHR | 50 % WHR / 50 % aux boiler |

| Simple pay-back | 5–6 yr | 4–5 yr |

(Proprietary heat balances withheld; numbers rounded to 5 % bands.)

6 FAQ – what non-engineers ask most

Q: What exactly is C/C?

Short answer: Clinker mass ÷ cement mass; 0.65 means 650 kg clinker per tonne cement.

Q: Can India finance small kilns?

Short answer: Yes—SIDBI Green-Equipment loans ≤ 8 % for projects < ₹150 cr.

Q: Is capture ever net-negative?

Short answer: Yes—if kiln fuel is biogenic; CAPEX similar, credits far higher.

Q: Will hydrogen prices affect kiln capture?

Short answer: Not until hydrogen < US $1 kg⁻¹; CEEW shows capture beats CCU fuels until that threshold.

7 Key take-aways

- Policy now has hard numbers: India’s draft C/C ≤ 0.65; UAE wants 14 Mt captured by 2030.

- Waste-heat trumps new boilers: up to 20 % steam saved.

- Net capture cost: large retrofits clear at US $35–55 t⁻¹ after tax perks.

- Five-year pay-backs already real when food-grade or EOR off-takes exist + concessional finance.

Need a kiln-specific decarb plan?

- Book your 30-min consult

- e-mail sales@ssgaslab.com

- or call +91-124-46 XXXXX

References

- BIS draft amendment IS 269 (OPC-43).

- UAE Net-Zero 2050 Strategy update.

- WHR case study, Sharjah Cement (2015).

- IEA CCUS cost curves, 2024.

- Hard-to-abate residual share (56 %) & hydrogen threshold, CEEW 2025 report.